All Categories

Featured

Table of Contents

Similar to other life insurance policy policies, if your customers smoke, utilize various other kinds of cigarette or nicotine, have pre-existing wellness problems, or are male, they'll likely have to pay a higher price for a last cost policy (final expense insurance company). Moreover, the older your customer is, the greater their price for a strategy will be, considering that insurer think they're handling even more risk when they provide to guarantee older clients - final funeral insurance.

The plan will also remain in force as long as the insurance holder pays their premium(s). While several other life insurance plans may require medical tests, parameds, and attending doctor statements (APSs), last expenditure insurance policy plans do not.

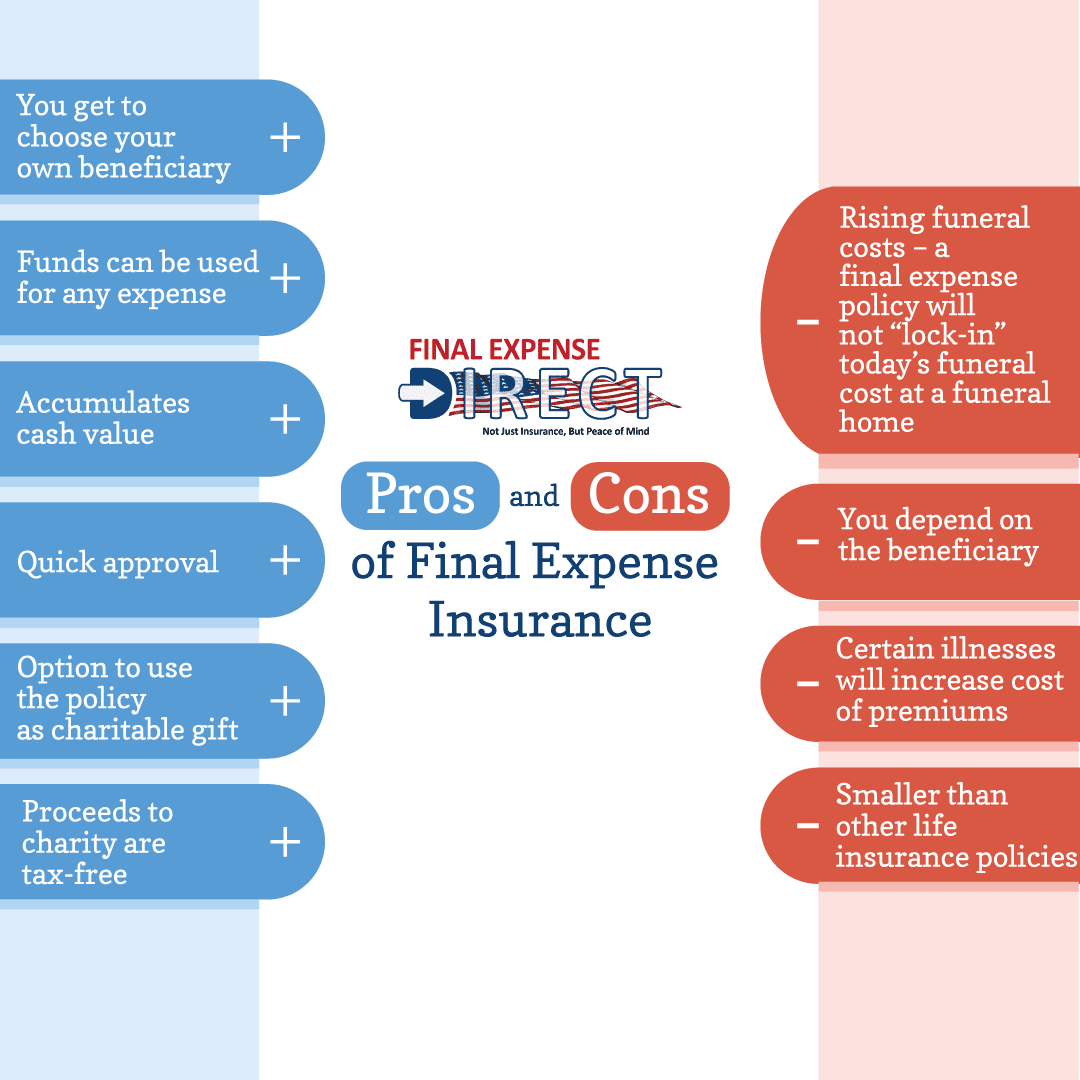

Funeral Burial Insurance

Simply put, there's little to no underwriting called for! That being said, there are two major sorts of underwriting for final cost strategies: streamlined issue and ensured problem. final expense care. With streamlined problem plans, customers typically just need to address a couple of medical-related questions and may be denied insurance coverage by the service provider based on those solutions

For one, this can permit representatives to determine what kind of plan underwriting would function best for a certain customer. And 2, it aids representatives limit their client's alternatives. Some carriers may invalidate clients for insurance coverage based on what medications they're taking and for how long or why they have actually been taking them (i.e., upkeep or therapy).

Senior Life Burial Insurance

The short solution is no. A final expense life insurance policy plan is a kind of irreversible life insurance policy policy. This implies you're covered until you pass away, as long as you have actually paid all your premiums. While this plan is developed to aid your recipient pay for end-of-life costs, they are cost-free to use the death advantage for anything they require.

Much like any type of various other long-term life plan, you'll pay a normal premium for a final expense plan in exchange for an agreed-upon fatality benefit at the end of your life. Each service provider has different regulations and options, yet it's relatively very easy to manage as your beneficiaries will certainly have a clear understanding of just how to invest the cash.

You may not need this kind of life insurance policy (aarp final expense insurance). If you have irreversible life insurance policy in position your last costs might currently be covered. And, if you have a term life policy, you might be able to transform it to a long-term policy without some of the extra actions of obtaining final cost coverage

Best Final Expense Policies

Designed to cover limited insurance requirements, this kind of insurance coverage can be an economical alternative for individuals that merely intend to cover funeral expenses. Some policies may have limitations, so it is necessary to review the fine print to be certain the policy fits your requirement. Yes, of course. If you're trying to find a long-term alternative, global life (UL) insurance policy remains in position for your entire life, as long as you pay your premiums.

This option to final expense coverage gives alternatives for added household protection when you need it and a smaller sized protection amount when you're older. whole life burial insurance for seniors.

5 Essential facts to bear in mind Preparation for end of life is never ever pleasant. Yet neither is the thought of leaving loved ones with unforeseen costs or financial debts after you're gone. In a lot of cases, these financial obligations can hold up the settling of your estate. Take into consideration these five facts concerning last expenditures and how life insurance policy can aid pay for them - final insurance plan.

{kind=link}

Latest Posts

Burial Insurance Quotes For Seniors

Final Expense Companies

How To Sell Final Expense Insurance